TL;DR: Cash-on-cash return (CoC) is a quick levered cash-yield metric. Use it to screen deals, but always pair it with IRR, DSCR, and unlevered metrics like cap rate or yield on cost for a complete picture.

What Is Cash-on-Cash Return?

Cash-on-Cash Return (CoC) measures the annual pre-tax cash flow you receive relative to the cash you put into the deal.

Formula:

CoC = Annual Pre-Tax Cash Flow ÷ Total Cash Invested

- Annual Pre-Tax Cash Flow: Gross scheduled rent + other income − vacancy/credit loss − operating expenses − total debt service (principal + interest), before taxes.

- Total Cash Invested: Down payment + closing costs + loan fees/points + initial reserves/escrow + upfront repairs or capex (excluding amounts financed).

Example

If you invest $100,000 cash (down payment + closing + repairs) and the property generates $8,000 in annual pre-tax cash flow, your CoC return is:

$8,000 ÷ $100,000 = 8%

Is CoC the Same as Cap Rate?

No.

- Cap rate is an unlevered yield: NOI ÷ purchase price.

- Cash-on-Cash return is a levered yield: actual cash flow after debt service ÷ cash invested.

Think of cap rate as how the asset performs; CoC as how your financing and investment structure perform.

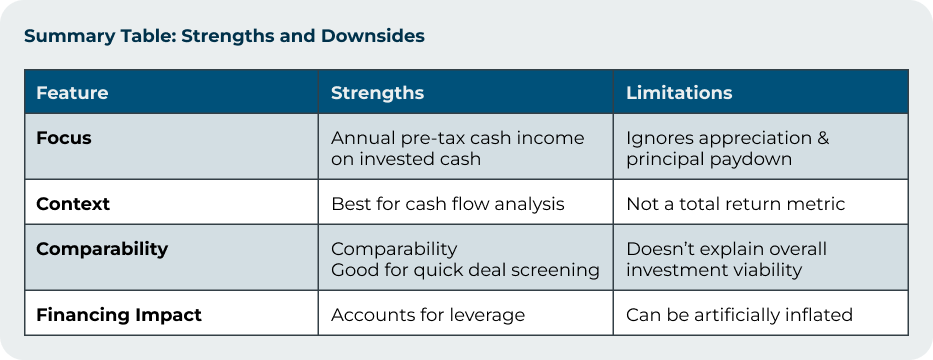

Key Benefits of Cash-on-Cash Return

- Simple and intuitive: Easy to calculate for quick deal screening.

- Cash-focused: Highlights actual dollars in your pocket, not paper gains.

- Leverage-sensitive: Shows how financing impacts investor returns.

Where Does CoC Fall Short?

- Ignores appreciation & amortization: Property value growth and principal paydown don’t show up.

- Not a total return metric: Leaves out tax benefits, exit proceeds, and equity build-up.

- Easily manipulated: Higher leverage or interest-only loans can inflate CoC — but add risk.

- Short-term snapshot: Reflects one year, which may be distorted by unusual repairs or tenant turnover.

When Should You Ignore a “Great” CoC?

- Aggressive leverage: High LTV, interest-only loans boost CoC but reduce safety. Check DSCR ≥ 1.20–1.30.

- Deferred maintenance: A roof or HVAC replacement will crush CoC. Always underwrite reserves for replacements.

- Floating-rate debt: Rising rates can shrink cash flow quickly. Stress-test ±200 bps.

When Is CoC Most Useful?

- Quick deal screens: Early-stage analysis to weed out poor performers.

- Comparing like-for-like properties: Works well when debt terms and capex needs are similar.

- Cash-flow-focused investors: Ideal if your goal is steady income, not long-term appreciation.

What Metrics Should You Pair With CoC?

- IRR (Internal Rate of Return): Captures timing and exit assumptions.

- Equity Multiple: Total return on invested capital over the life of the deal.

- Cap Rate & Yield on Cost: Unlevered measures for apples-to-apples property comparisons.

- DSCR (Debt-Service Coverage Ratio): Assesses ability to cover mortgage with NOI.

- Break-even Occupancy: Shows how low occupancy can fall before you go negative.

A Worked Mini-Example

Scenario 1: Fully Amortizing Loan

- Purchase price: $1,000,000

- 70% LTV loan at 6.5%, 30-year amortization

- Total cash invested: $340,000 (down + costs + repairs)

- NOI: $59,000

- Debt service: $75,800

- Annual pre-tax cash flow: −$16,800 → CoC = −4.9%

Scenario 2: Interest-Only Loan (Same Deal)

- Debt service: $45,500

- Annual pre-tax cash flow: +$13,500 → CoC = +4.0%

Same building, same NOI, radically different CoC depending on financing terms.

Practical Advice

- Standardize your assumptions. Always disclose: vacancy rate, reserves, debt terms, and what you include in “cash invested.”

- Look at multi-year CoC. Year-1 may mislead. Track CoC from Year-1 through Year-5 to see rent bumps, amortization, and expense creep.

- Separate financing events. Don’t treat a cash-out refinance as “cash flow.” Model it separately in IRR/equity multiple.

- Check multiple metrics. CoC by itself can’t tell you if the deal is safe or scalable. Pair it with DSCR, cap rate, and IRR.

Bottom Line

Cash-on-cash return is a powerful screening tool for cash-flow-driven investors. But it’s just one piece of the puzzle. To make sound real estate decisions:

- Pair CoC with IRR, equity multiple, cap rate, and DSCR.

- Look beyond Year-1 and account for reserves and future capital needs.

- Treat CoC as a quick test, not the final word.

A “great” CoC on paper could mean great cash flow — or hidden risk. The difference is in your underwriting.

Ready to Apply This to Real Deals?

Understanding cash-on-cash return is only the first step. The real edge comes from knowing how to blend CoC with advanced metrics like IRR, DSCR, and equity multiple to evaluate risk and maximize returns.

📞 Book a 1:1 call with Michael Pouliot, our CIO, to walk through real investment scenarios and see how professional investors underwrite deals. Whether you’re refining your strategy or evaluating your next acquisition, this conversation will give you actionable insights to make smarter, safer investment decisions.

CLICK HERE to book your call with Michael

.svg)