Market Overview

The second half of 2025 signals a cautiously optimistic yet evolving landscape for the U.S. multifamily sector. After weathering a period marked by record-breaking supply and macroeconomic volatility, the market is stabilizing as new construction slows and demand remains resilient.

Strong Demand, Moderating Supply

Demand for multifamily rental housing continues to hold firm, supported by strong demographic drivers and the persistent affordability gap between renting and homeownership.

New completions peaked in 2024 at approximately 608,000 units—the highest level in nearly four decades—creating temporary oversupply in many markets. In 2025, deliveries are projected to decline sharply, with 300,000–350,000 new units expected by year-end. This slowdown will ease supply-side pressures, particularly in overbuilt regions.

Rent and Vacancy Dynamics

- Rent Growth: Average U.S. rent growth for 2025 is projected at 2.2%, below the long-term annual average of 2.8%, but still positive.

- Vacancy Rates: National vacancy is expected to edge higher to around 6.2%, compared to a historical average of roughly 5.5%.

These figures reflect a market transitioning toward equilibrium after a period of rapid expansion.

Cap Rates and Investment Activity

Cap rates have stabilized after prior expansion, even as interest rates remain relatively elevated. Investor sentiment is gradually improving, with multifamily transaction volume projected to reach $370–$380 billion in 2025, supported by pent-up deal flow and increasingly competitive pricing as H2 progresses.

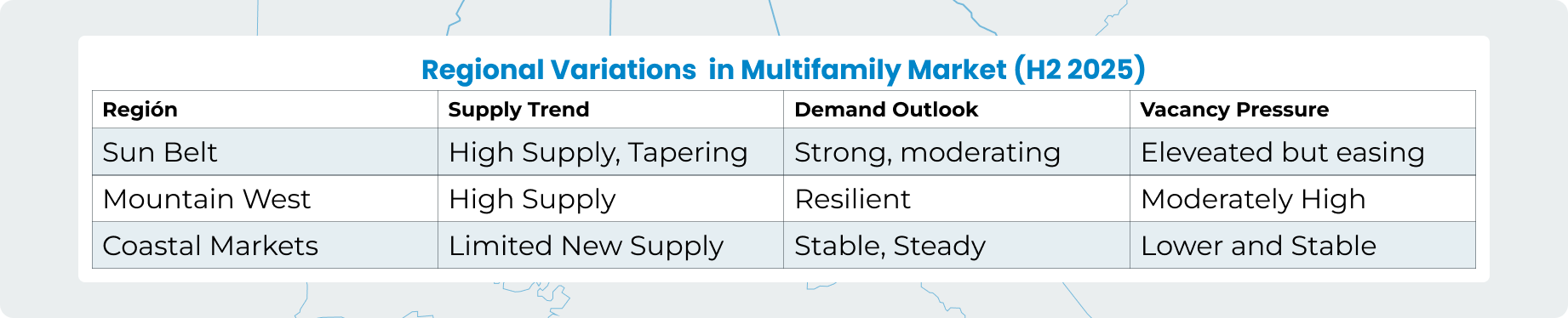

- Oversupplied metros—such as Austin, Dallas, and Atlanta—saw double-digit vacancy in early 2025 but should benefit from reduced completions in H2.

- Coastal and low-supply markets are expected to outperform in both rents and occupancy.

Key Forces Shaping H2 2025

Interest Rates

Borrowing costs remain a challenge. While the Federal Reserve is expected to begin easing rates later in the year, the pace and magnitude of cuts remain uncertain, impacting asset values and debt-driven acquisitions.

Operating Margins

Property owners face margin compression from subdued rent growth and elevated expenses. This environment is driving a focus on operational efficiency, data-driven pricing strategies, and improved resident experiences.

Technology Adoption

Apartment operators are leveraging analytics, real-time data, and smart automation to enhance leasing, optimize risk management, and boost overall portfolio performance.

Risks and Opportunities

Risks

- Persistently high interest rates or an economic downturn could pressure valuations and slow rent growth.

- Rising insurance costs and regulatory uncertainty add complexity to expense management.

Opportunities

- A sharp reduction in new starts and deliveries is setting the stage for a healthier supply-demand balance, particularly as early H2 leasing absorbs excess inventory.

- Strategic acquisitions in underbuilt markets, portfolio repositioning, and tech-driven asset management remain key levers for growth.

Bottom Line

The multifamily sector in H2 2025 is characterized by stabilization, careful optimism, and operational discipline. While challenges persist—especially around costs and macroeconomic uncertainty—the long-term outlook remains favorable for well-capitalized owners and forward-thinking operators. Expect a market that rewards agility, technology adoption, and strategic positioning as it transitions to a new equilibrium.

Ready to Capitalize on the H2 2025 Multifamily Opportunity?

Click here to book a 15-minute strategy call with our CIO, Michael Pouliot.

.svg)