Introduction: The Language of Institutional Trust

Institutional capital doesn't chase narratives. It follows numbers.

When a family office evaluates a multifamily sponsor, or when an RIA considers allocating client capital to a private real estate fund, the conversation revolves around metrics. Not vague projections or optimistic pro formas, but verifiable, auditable data points that demonstrate execution capability, downside protection, and operational discipline.

The difference between raising $5 million from friends and family versus $50 million from institutional sources often comes down to fluency in this language. Sophisticated LPs have seen enough pitch decks to know when a sponsor is guessing versus when they're operating with institutional rigor.

At Carbon, managing over 2,000 units across multiple markets has taught us that the metrics institutional allocators care about fall into three categories: financial performance indicators that prove cash flow stability, operational benchmarks that demonstrate execution capability, and portfolio-level analytics that show risk management discipline. Master these, and you transform from a hopeful sponsor into a credible institutional partner.

This essay breaks down the specific metrics that matter, why they matter, and how to present them in ways that build confidence rather than concern.

Financial Performance: The Foundation of Credibility

Debt Service Coverage Ratio: The First Line of Defense

No metric carries more weight with institutional LPs than Debt Service Coverage Ratio (DSCR). This simple calculation, Net Operating Income divided by debt service, tells lenders and investors whether a property generates enough cash flow to cover its loan payments with room to spare.

Institutional lenders typically require a minimum DSCR of 1.25x for agency debt. This means the property must generate $1.25 in NOI for every dollar of debt service. Why this threshold? Because it provides a cushion against occupancy dips, unexpected expenses, or market softness without triggering a default.

When DSCR falls below 1.20x, sophisticated LPs start asking pointed questions. When it drops below 1.10x, alarm bells sound. A property operating at 1.05x DSCR is one bad quarter away from a coverage violation, which can trigger acceleration clauses or force asset sales at inopportune times.

The best sponsors don't just report current DSCR. They model it across multiple scenarios: base case, stressed occupancy, elevated interest rate environment. This forward-looking approach demonstrates that you understand risk, not just opportunity.

Cash-on-Cash Return: Separating Real Yield from Paper Gains

Cash-on-Cash (CoC) return measures the actual cash distributed to equity investors relative to the cash they invested. Unlike IRR, which can be manipulated through timing assumptions or theoretical appreciation, CoC reflects money that actually lands in investor accounts.

Institutional allocators scrutinize CoC because it reveals operational execution. A sponsor promising 8% annual CoC but consistently delivering 6% is either overly optimistic or operationally inefficient. Conversely, a sponsor who underwrites conservatively at 6% and delivers 7-8% builds a track record of exceeding expectations.

The critical insight: CoC should stabilize and potentially grow over the hold period. Properties in their first 18 months post-acquisition naturally show lower CoC as value-add work gets implemented. By year three, CoC should reflect stabilized operations. If it doesn't, something is wrong with the business plan or the execution.

At Carbon, we've learned that consistent CoC delivery builds more LP confidence than promising outsized returns. When you underwrite at 6% and deliver 7% for three consecutive years, re-raising capital becomes exponentially easier.

Expense Ratio: The Efficiency Benchmark

Expense ratio, calculated as operating expenses divided by gross potential rent, reveals operational efficiency. Institutional allocators compare this metric across properties and markets to identify outliers.

Well-managed Class B and C multifamily typically runs expense ratios between 35% and 45%. Properties significantly above this range signal operational problems: overstaffing, poor vendor relationships, or deferred maintenance creating emergency repairs.

The nuance matters. A property in Minneapolis will naturally run higher expenses than one in Phoenix due to snow removal and heating costs. Sophisticated LPs understand this and benchmark against market-specific norms, not arbitrary national averages.

More important than the absolute number is the trend. If expenses as a percentage of revenue are climbing year over year without corresponding improvements in property condition or resident satisfaction, you have an execution problem. If expenses are declining while occupancy remains strong, you're demonstrating operational excellence.

Carbon's vertical integration strategy, including our own property management platform, allows us to maintain expense ratios at the lower end of market ranges. This operational efficiency translates directly into higher NOI and stronger distributions, which sophisticated LPs immediately recognize in our quarterly reporting.

Operational Benchmarks: Proving Execution Capability

Occupancy and Turnover: The Health Indicators

Physical occupancy tells part of the story. Economic occupancy tells the full story. A property showing 95% physical occupancy but 88% economic occupancy (due to concessions, bad debt, or down units) is masking operational challenges.

Institutional LPs focus on economic occupancy because it directly impacts NOI. They also track turnover rates closely. Annual turnover above 60% in a stabilized Class B property signals resident dissatisfaction, poor leasing execution, or market weakness. Turnover below 40% suggests strong operations and resident retention.

The cost of turnover is substantial. Between lost rent during vacancy, make-ready expenses, leasing commissions, and administrative costs, each turn can cost $2,000 to $4,000 per unit. High turnover quietly erodes NOI and compresses returns.

Carbon's focus on resident experience and quality renovations has kept our turnover rates below market averages. This operational discipline shows up in our quarterly reports as stronger occupancy, lower turnover costs, and more predictable cash flow, all metrics that institutional capital rewards.

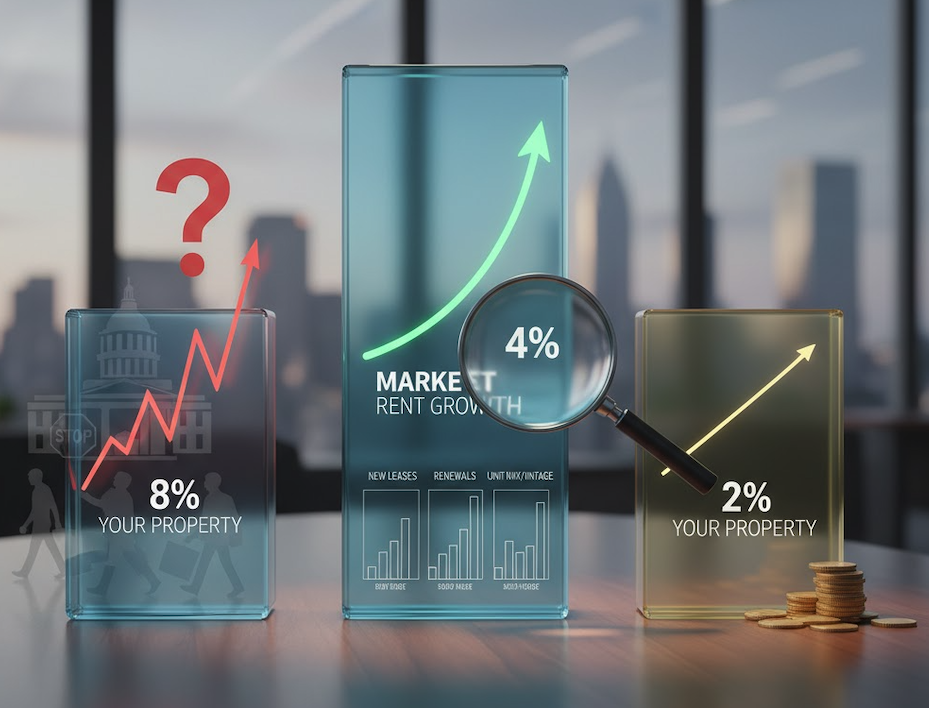

Rent Growth and Market Positioning

Rent growth over time demonstrates that you're capturing market momentum without pushing residents out. Institutional allocators want to see rent increases that track or slightly exceed market, not wild swings that suggest pricing errors.

A property showing 8% annual rent growth in a market growing at 4% raises questions. Are you displacing long-term residents? Will you face pushback from city officials? Are you creating turnover problems? Conversely, if market rents are growing 5% annually but your property only achieves 2%, you're leaving money on the table.

The best sponsors segment rent data: new leases versus renewals, unit mix, and vintage. This granularity shows you understand your pricing power at the unit level, not just property-wide averages.

Capital Expenditure Tracking: The Proof of Discipline

Institutional LPs scrutinize CapEx deployment because it reveals whether sponsors execute on their business plans or drift into scope creep. When a sponsor budgets $15,000 per unit for renovations and consistently spends $18,000, that's a red flag about underwriting accuracy and cost control.

The best reporting breaks CapEx into categories: unit interiors, common areas, building systems, and deferred maintenance. This transparency allows LPs to understand where capital is going and why. It also demonstrates that the sponsor isn't just throwing money at problems but executing a strategic value-add plan.

At Carbon, we learned early that CapEx tracking needs to be real-time, not retrospective. Monthly draws against construction budgets, unit-level completion tracking, and variance analysis keep projects on schedule and on budget. When we present quarterly reports to LPs, they can see exactly how capital is being deployed and what NOI lift we're achieving per dollar spent.

Risk Management: The Portfolio View

Vintage Diversification: The Cycle Buffer

Sophisticated allocators evaluate portfolio construction, not just individual deals. One of the most important portfolio metrics is vintage diversification, or the distribution of acquisitions across different market cycles.

A sponsor who deployed all capital in 2021-2022, when valuations peaked and leverage was cheap, faces concentrated risk. If those properties need to be refinanced in a higher rate environment or sold in a softer market, the entire portfolio could underperform simultaneously.

Conversely, a sponsor with acquisitions spanning 2018, 2020, 2022, and 2024 has natural diversification. Some properties entered at lower basis with favorable debt structures. Others may have shorter-term holds but stronger near-term cash flow. This spread reduces portfolio-level risk.

Carbon's acquisition pace has created natural vintage diversification. Our earliest deals, acquired at lower valuations with longer-term agency debt, provide stability. More recent acquisitions, while at higher entry prices, capture current rent growth and position us for the next cycle.

Geographic Concentration: Balancing Focus and Diversification

Institutional allocators want to see enough geographic diversification to mitigate local market risk without spreading so thin that operational quality suffers. A sponsor with 2,000 units spread across 15 markets likely lacks the boots-on-the-ground presence to manage effectively. One with 2,000 units in a single tertiary market faces catastrophic risk if that economy stumbles.

The sweet spot for most multifamily sponsors is three to five core markets where they have deep relationships, local expertise, and enough scale to justify dedicated personnel. This concentration allows operational efficiency while providing geographic risk mitigation.

At Carbon, our focus on secondary Sun Belt markets provides diversification without dilution. We're not trying to be everywhere. We're building depth in markets where fundamentals support long-term rent growth and where our operational model delivers competitive advantage.

Leverage Analysis: Debt Structure as Risk Management

LPs don't just care about total leverage (loan-to-value). They care about debt structure: fixed versus floating rates, interest-only periods, maturity schedules, recourse versus non-recourse terms, and prepayment flexibility.

A portfolio where 70% of debt matures in the same 12-month window creates refinancing risk. If rates have moved against you or if the property underperformed, you face a forced recapitalization at unfavorable terms. Staggered maturities spread this risk across time.

Similarly, a portfolio heavily weighted toward floating-rate debt in a rising rate environment demonstrates poor risk management. Institutional capital wants to see sponsors who understand duration risk and structure debt to match hold periods and business plans.

Carbon's preference for agency debt with fixed rates and staggered maturities reflects this discipline. We're not maximizing leverage for the sake of paper returns. We're building a capital structure that can withstand stress without forcing asset sales or equity calls.

Reporting Standards: Making Metrics Actionable

Frequency and Transparency: The Trust Multiplier

How you report matters as much as what you report. Institutional LPs expect quarterly reporting at minimum, with trailing 12-month data, year-over-year comparisons, and variance analysis against projections.

The best sponsors provide:

- Property-level P&L statements showing revenue, expenses, NOI, and cash flow

- Occupancy and leasing metrics with market comparisons

- CapEx tracking against budget with completion percentages

- Debt service coverage calculations

- Distribution history and future projections

Transparency around challenges builds more credibility than only highlighting wins. When occupancy dips, expenses spike, or timelines slip, sophisticated LPs want to know why, what you're doing about it, and how it affects returns. Hiding problems erodes trust. Addressing them proactively builds confidence in your crisis management capability.

Benchmarking Against Market: The Context That Matters

Raw numbers without context mean little. A property showing 4% rent growth might be excellent in a flat market or disappointing in a hot one. Institutional allocators want to see how your performance compares to market benchmarks.

This means including third-party data: CoStar rent growth trends, CBRE occupancy statistics, or local economic indicators. When your metrics track or exceed market, that demonstrates execution. When they lag, you need to explain why and what you're doing to close the gap.

Carbon uses market data extensively in our reporting. When we show LPs that our properties are outperforming market averages on occupancy, rent growth, and expense management, it validates our operational thesis and justifies continued capital deployment.

The Green Street Lens: Institutional-Grade Valuation Discipline

For sponsors seeking to professionalize their investor communications, understanding how firms like Green Street Advisors think about valuations provides critical insights.

Green Street, one of the most respected research firms in commercial real estate, pioneered Net Asset Value (NAV) analysis, which values portfolios based on underlying property fundamentals rather than stock prices or book values. Their methodology focuses on stabilized NOI, market cap rates, and rigorous assumptions about reversion values.

When institutional allocators evaluate multifamily sponsors, they often apply similar frameworks:

- What's the property worth today based on current NOI and market cap rates?

- What's the realistic exit cap rate assuming mean reversion?

- How sensitive is valuation to occupancy, rent growth, or expense inflation?

- What does the distribution waterfall look like under various exit scenarios?

Sponsors who model exits using conservative reversion cap rates (typically 25-50 basis points above entry) signal sophistication. Those who assume cap rate compression or rely on aggressive appreciation to hit return targets raise red flags.

At Carbon, we underwrite conservatively, often assuming flat or compressed cap rates at exit. This discipline ensures our projected returns are achievable through operational performance rather than market speculation. When we exceed those projections through better-than-expected NOI growth or favorable exit timing, it reinforces credibility.

Technology and Data: The New Table Stakes

Institutional capital increasingly expects sponsors to leverage technology for better decision-making and reporting. This doesn't mean expensive enterprise software. It means having systems that provide real-time visibility into portfolio performance.

Property management platforms like Yardi or RealPage allow sponsors to track unit-level metrics, automate reporting, and identify operational trends before they become problems. Business intelligence tools like Tableau or PowerBI transform raw data into visual dashboards that make performance instantly understandable.

The sponsors who win institutional mandates are those who can answer questions with data, not anecdotes. When an LP asks about maintenance costs per unit or vacancy days per turn, you should be able to provide precise answers within minutes, not promises to follow up after digging through spreadsheets.

Carbon's investment in operational systems reflects this reality. Our internal dashboards track metrics across the portfolio in real time, allowing us to spot issues early and report performance with confidence. This operational transparency has become a competitive advantage in capital raising.

Alignment: The Ultimate Metric

No metric matters more to institutional capital than alignment. Are the sponsor's incentives structured to prioritize LP returns, or does the waterfall structure encourage excessive risk-taking or premature exits?

Sophisticated allocators scrutinize promote structures carefully. A 70/30 split after an 8% preferred return represents strong alignment. A 50/50 split after a 6% pref with a catch-up provision dilutes LP economics. Zero sponsor co-investment raises questions about skin in the game.

The best sponsors don't just invest meaningful personal capital alongside LPs. They also structure waterfalls that reward patient, risk-adjusted returns rather than quick flips. They report distributions clearly, showing how much came from operations versus refinancings or sales. They communicate honestly about how sponsor compensation is earned and when it's received.

At Carbon, we've always believed that the best way to attract institutional capital is to act like an institution ourselves: disciplined underwriting, conservative leverage, transparent reporting, and alignment that puts LP interests first. This philosophy has allowed us to raise capital from family offices and institutional sources who value execution over promises.

FAQs

What's the minimum portfolio size needed to attract institutional capital?

Most institutional allocators look for sponsors managing at least $50-100 million in assets, though this varies by LP type. Family offices may invest earlier in a sponsor's track record if the fundamentals and team are strong. The key is demonstrating you have systems and processes that can scale, not just a collection of one-off deals.

How do institutional LPs evaluate sponsors who are scaling rapidly?

Rapid growth raises both opportunity and risk flags. LPs want to see that you're scaling infrastructure alongside portfolio size: adding experienced personnel, implementing better systems, maintaining underwriting discipline. Growth that outpaces operational capability creates disaster risk. Growth that maintains quality and consistency builds confidence.

What's the single most important metric for multifamily sponsors?

If forced to choose one, most institutional allocators would point to Debt Service Coverage Ratio. It's the clearest indicator of cash flow stability and default risk. A portfolio running DSCR above 1.30x across multiple properties and vintages demonstrates operational excellence and conservative capital structure.

How should sponsors report on properties that are underperforming?

With transparency and a clear action plan. Sophisticated LPs understand that not every property performs as projected. What matters is how quickly you identify problems, how honestly you communicate them, and how effectively you execute solutions. Sponsors who try to hide underperformance until it becomes catastrophic lose trust permanently.

Do institutional LPs prefer sponsors who use property management companies or self-manage?

It depends on scale and capability. At smaller portfolios, third-party management often makes sense. As you approach 1,000+ units, vertical integration (self-management) typically improves operational performance and economics. What matters most is demonstrable operational excellence, regardless of management structure. LPs care about results, not philosophy.

Conclusion: Precision as Strategy

The metrics that win over institutional capital aren't mysterious or arbitrary. They reflect decades of hard-won experience by sophisticated allocators who have seen sponsors succeed and fail across multiple cycles.

Master these metrics not because they impress investors, but because they force operational discipline that creates real value. When you obsess over DSCR, you build cushion against downside. When you track expense ratios monthly, you catch cost creep early. When you report transparently, you build trust that survives inevitable challenges.

The sponsors who scale from friends-and-family money to institutional mandates share a common trait: they treat every dollar of LP capital with fiduciary-level care, measured through metrics that reveal truth rather than stories.

At Carbon, this discipline isn't marketing. It's culture. It's how we've built credibility with institutional sources who value execution over promises. And it's the framework we use to evaluate our own performance, holding ourselves accountable to standards that ensure we're building wealth for our investors, not just collecting fees.

The next generation of great multifamily operators won't be those with the best pitch decks or the flashiest returns. They'll be the ones who master the language of institutional capital and let their metrics do the talking.

Subscribe for Institutional-Grade Insights

Join Carbon's private investor newsletter for monthly analysis on multifamily metrics, market intelligence, and operational best practices at https://www.investwithcarbon.com/newsletter

Sources

National Multifamily Housing Council (NMHC), 2024 Apartment Operations Report

Urban Land Institute (ULI), Emerging Trends in Real Estate 2025

Green Street Advisors, Real Estate Analytics Methodology

Freddie Mac Multifamily, Small Balance Loan Program Guidelines 2024

CBRE Research, U.S. Multifamily Investment Trends 2024

National Apartment Association (NAA), Survey of Operating Income and Expenses 2024

Preqin, Private Real Estate Investor Preferences Report 2024

PGIM Real Estate, Global Outlook 2025

Marcus & Millichap, Multifamily Investment Forecast 2024-2025

RealPage Analytics, Market Rent Growth and Occupancy Trends Q4 2024

.svg)